My Kids are Getting Social Security Survivors' Benefits: Here's How That Works and How We’re Investing It

I thought documenting some of the financial steps after death would be helpful to someone else who loses a spouse, so I’m writing a couple entries on my experience here.

During the burial planning process, Newton Bracewell kindly gave us a sheet discussing what survivor benefits (if any) might be available for a family. When a parent or spouse passes away, meeting with Social Security isn’t at the top of anyone’s priorities list, but it is important as one of the financial next steps when someone dies. I scheduled an appointment (availability is pretty limited) a couple of weeks out.

Britney stayed at home as soon as we had kids, and I wasn’t sure what (if anything) would be available for them. It turns out she would not have qualified for retirement benefits, but did qualify for death benefits: You need one quarter of work for each year over age 21 you are to be eligible. Her prior work experience qualified the kids for survivors’ benefits, and a one-time payment of $255 to me. Had our income been below the poverty level, we may have gotten an extra monthly draw (I’m thankful that’s not our situation).

The paperwork was pretty straightforward- names, marriage cert, birth certs, and receiving accounts were required. You can find the list online at https://www.ssa.gov/survivor

The Chico SSA Office at 1370 E Lassen Ave #150, Chico, CA 95973

The payments came through within a week of applying. The kids are getting over $400/mo. until they turn 18 or graduate high school (whichever comes later). I’m not certain what happens if they get held back or don’t graduate, but we’ll hope that doesn’t come into play.

Giving a 7-year-old $400 a month doesn’t seem like a great idea (he’d convert it all to Roblox in-game money, I’m certain). Instead, we directed it to their investment (taxable brokerage) accounts. On the 20th of each month, money will go in, and on the 22nd, it’ll auto-invest into an all-stock portfolio.

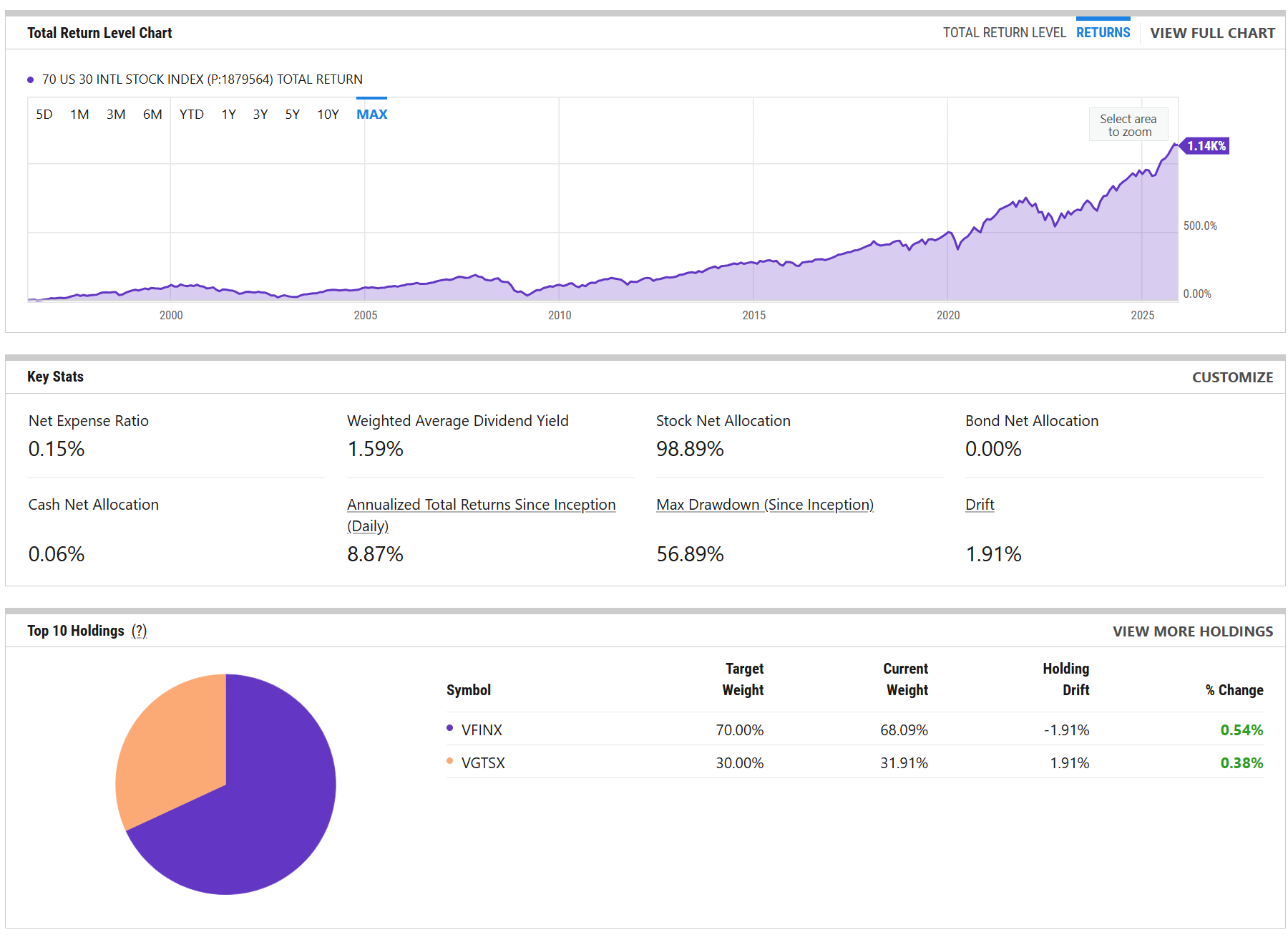

The portfolio is blended between 2 funds (70% US index fund, 30% in an International one) for multiple reasons:

Owning stock in companies has, over long time periods, historically provided higher returns than bonds/cash and beat inflation. We understand and accept market risk.

The kids won’t be touching this money for several years (they already have 529 college funds for ages 19-22)

You can’t automate monthly ETF purchases, only mutual funds.

Index funds carry low fees and can be hard to beat for growth-oriented investors.

Index funds rarely (if ever) pay unwanted capital gain distributions, which could trigger a kiddie tax issue.

US companies make up around 70% of the global market cap, international companies make up the other 30%.

US stocks have been on an absolute tear these past 15 years, but history shows international stocks can do quite well when us markets slow down (diversification!)

Overall, this portfolio has averaged 8.87% annual returns since 1996. I don’t know if returns will be similar in the future, but 3 decades is a pretty long sample size to draw from

Obvious disclosures. Investing involves all types of risk. This is a backwards looking snapshot, and past performance doesn’t guarantee future results. This is not a proposal or recommendation: My choices are my own and will likely not be exactly right for anyone else!

That’s our experience and plan so far. Obviously, we’d all prefer not to be in this situation, but it’s good to know that Social Security isn’t some black hole for people who paid into it during their lifetimes.