3 Things We're Skeptical on: June 2025 Edition

Here are a few pitches we’re not swinging at these days:

Claim: Artificial Intelligence is Going To Send Unemployment to 20%

“AI is starting to get better than humans at almost all intellectual tasks, and we’re going to collectively, as a society, grapple with it,” -Anthropic CEO Dario Amodei

Leave it to an AI CEO to claim his product is going to displace 30+ million jobs!

Amodei believes the AI tools that Anthropic and other companies are racing to build could eliminate half of entry-level, white-collar jobs and spike unemployment to as much as 20% in the next one to five years, he told Axios

I’m not an expert in these things, so I won’t be nearly as critical as Ed Zitron was in his viral post “Reality Check”. But I’ll make a few random points and you can connect your own dots:

Builder.ai is a unicorn company that just went bankrupt when it was revealed it was just Indian coders doing the legwork

So was Amazon’s “Just Walk Out” technology: 1,000 Indian workers just watched you shop and they called it ‘AI’

Open AI Spent 9 Billion to lose 5 Billion in 2024.

Open AI raised $40 Billion at a valuation of $300 Billion. They can’t make the non-profit thing work (not profitable) so now they’re converting to for-profit so they can sell equity.

Terrifying: This OPEN AI model was caught disobeying commands, sabotaging its code to prevent a future shutdown order

AI Models playing a game will resort to cheating/hacking opponents in order not to lose. Maybe we have more in common with the machines after all

When given a question it can’t answer, AI will often make up or ‘hallucinate’ responses

The list goes on.

Look, I have played with some amazing AI tools. The videos are amazing. Tech companies continue to make gigantic investments and grandiose promises about where we’re headed.

But the outputs aren’t exactly trustworthy. If you caught an employee performing half of the sins above, you’d fire them regardless of how cheap they were.

Furthermore, these businesses demand an awful lot of physical resources (electricity, minerals, water), and haven’t proven even close to self-sustaining/profitable (yet).

Conclusion: More jobs will require knowledge of how to use AI tools, but the AI isn’t ready to replace the labor force yet.

Private Credit & Private Equity Offerings

Here’s the call we’re receiving 5x a week. It’s some version of “Public equities can’t perform the way they have in the past, because lots of great companies are growing privately, longer”.

Therefore “Investors (clients) can earn more money while seeing less volatility with private investments”

Hypothetically, of course.

Here’s the chart from one Venture Capital firm 2022 pitchbook to hammer that idea home:

This idea seems attractive. There are a few problems with private equity pitches though:

Not every venture capital firm (there are hundreds, if not thousands now) is going to bet correctly on the next unicorn.

Even if that firm identifies one, not every private company wants to sell ownership to a private equity mutual fund (AKA ‘why wouldn’t I go with a superstar VC firm like Sequoia instead’)

We’ve noticed: Endowments are trying to sell stakes in their private funds. Harvard, Yale and New York City Pension are all unloading Billion-dollar private equity and private credit positions… and they need buyers. Why don’t they want to keep these investments?

Private credit: “Let’s loan money and expertise to businesses who couldn’t qualify for a normal bank loan or bond offering”. Yikes.

Getting money out of these funds means waiting quarters, years or decades. You can’t just sell your stake in the local laundromat the way you can shares of an index fund.

Lastly, and maybe most importantly: These funds carry high fees and leverage, which is great for the fund manager but not the investor. State Street did some research that showed (after fees and leverage) returns were roughly equal to public equities. Ouch:

Conclusions: I wish nothing but the best to these fund managers, but this isn’t particularly attractive from a risk/reward standpoint today given the drawbacks.

Treasury vs Corporate Bond Yield Spreads: Somebody is Probably Wrong

The bond market is an interesting place right now. There’s been an incredible demand for fixed income, and returns aren’t necessarily compensating investors for risks. For example, today, 10 year bonds look like this:

U.S. Treasury: 4.4%

AAA Corporate Bond: 4.62%

AA Corporate: 4.86%

A Corporate: 5.18%

BBB Corporate: 5.49%

So, you could buy US Treasuries (considered one of safest bonds worldwide) which is backed by world’s largest GDP and we print our own money. You get 4.4% annually.

Or, you could buy BBB corporate bonds, businesses that need money and are one level above “junk” rating, and get just 1% annually more.

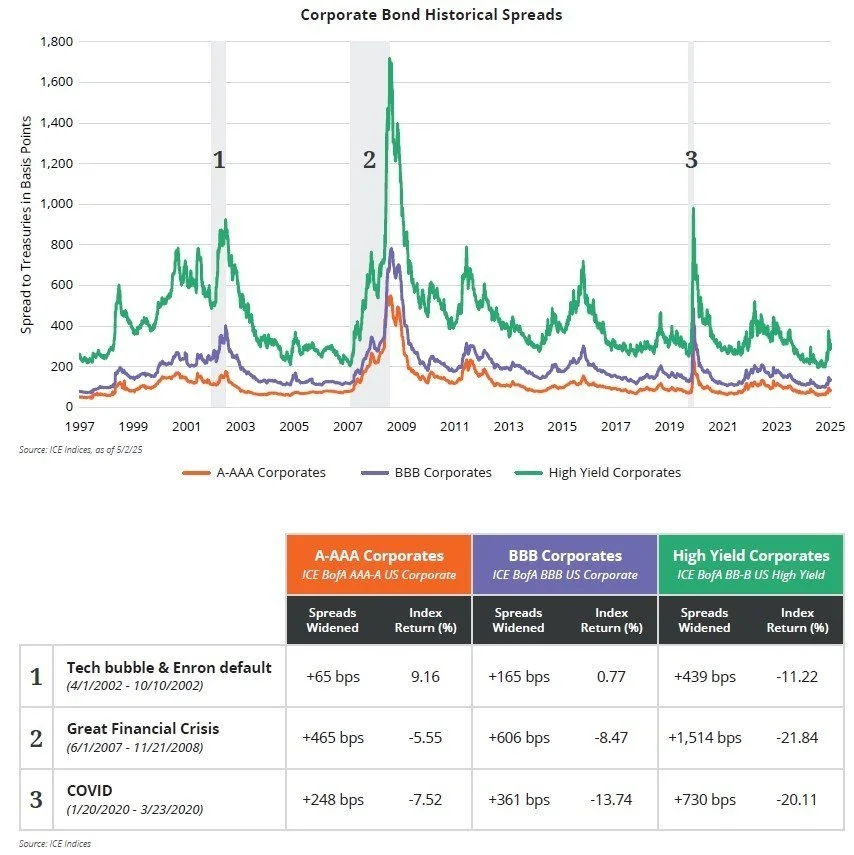

We don’t think the extra juice is worth the squeeze. Take a look at how high yield corporates performed in the last 3 crisis’:

For reference, the 10 year treasury actually gained in principal value during each of these panics!

Conclusion: we’re sticking mainly with treasuries for most investors until corporate bonds start paying a higher rate (to compensate for credit risk).